Personal finance and budgeting are crucial aspects of financial stability and long-term wealth creation. Managing money effectively helps individuals achieve their financial goals, avoid debt traps, and prepare for unforeseen expenses. This guide explores comprehensive strategies to master personal finance and budgeting.

2. Importance of Personal Finance

Helps in financial security and independence.

Enables smart decision-making for future investments.

Prevents overspending and unnecessary debt.

Prepares individuals for emergencies and retirement.

Enhances quality of life by reducing financial stress.

2.1 Key Components of Personal Finance

Component

Description

Income

Earnings from job, business, investments, etc.

Expenses

Regular spending like rent, food, utilities.

Savings

Money set aside for future needs.

Investments

Money allocated for wealth growth.

Debt Management

Handling loans and liabilities wisely.

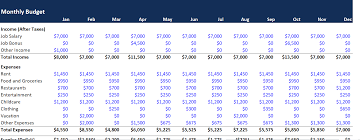

3. Understanding Budgeting

Budgeting is the process of planning and managing income and expenses to maintain financial balance. A well-structured budget helps in:

Tracking income and expenditures.

Prioritizing necessary expenses.

Avoiding financial strain.

3.1 Types of Budgets

Zero-Based Budgeting – Assigns every dollar to a specific expense or savings.

50/30/20 Rule – 50% on needs, 30% on wants, 20% on savings.

Envelope Budgeting – Allocating cash into separate envelopes for different expenses.

4. Income Management

Diversify income sources (salary, side hustles, investments).

Track monthly and annual income.

Allocate income wisely across different financial priorities.

Follow the Pay Yourself First method (set aside savings before spending).

Automate monthly savings.

Consider high-yield savings accounts.

6.1 Short-Term vs. Long-Term Savings

Type

Examples

Short-term

Emergency fund, vacation fund.

Long-term

Retirement, home down payment.

7. Investment Planning

Investing helps grow wealth over time and combats inflation.

Stocks & Bonds: High-risk, high-reward options.

Mutual Funds: Diversified investment option.

Real Estate: Long-term wealth-building asset.

Cryptocurrency: Emerging high-volatility market.

8. Debt Management

Prioritize high-interest debts first.

Use the Debt Snowball or Avalanche methods.

Consolidate loans for better interest rates.

8.1 Types of Debt

Type

Examples

Good Debt

Education loans, home mortgages.

Bad Debt

Credit card debt, payday loans.

9. Credit Score Optimization

Pay bills on time.

Reduce credit utilization below 30%.

Monitor and dispute credit report errors.

9.1 Credit Score Ranges

Score Range

Rating

300-579

Poor

580-669

Fair

670-739

Good

740-799

Very Good

800+

Excellent

10. Retirement Planning

Start early with 401(k), IRAs, or pension plans.

Diversify retirement funds.

Plan for inflation and healthcare costs.

11. Emergency Fund Creation

Save at least 3-6 months’ worth of expenses.

Keep funds in an easily accessible account.

Avoid using emergency savings for non-emergency needs.

12. Tax Planning & Optimization

Use tax-advantaged accounts (401(k), HSA, IRA).

Claim deductions and credits.

Plan business expenses efficiently.

13. Financial Goal Setting

Use SMART goals (Specific, Measurable, Achievable, Relevant, Time-bound).

Review and adjust goals periodically.

14. Smart Spending Habits

Implement the wait-before-you-buy strategy.

Compare prices and look for deals.

Avoid emotional spending.

15. Risk Management & Insurance

Get adequate health, life, auto, and home insurance.

Regularly review insurance policies.

16. Digital Tools & Apps for Finance

App

Purpose

Mint

Budget tracking

YNAB

Zero-based budgeting

Robinhood

Investment platform

17. Overcoming Common Financial Mistakes

Living paycheck to paycheck.

Not saving early.

Overspending on lifestyle inflation.

18. Psychological Aspects of Finance

Understand emotional spending.

Build discipline and financial confidence.

19. Teaching Financial Literacy to Kids

Introduce money management early.

Encourage saving and smart spending.

20. Conclusion & Final Thoughts

Mastering personal finance and budgeting is key to financial freedom. With proper planning, disciplined savings, and smart investing, individuals can achieve their financial goals and live a stress-free life.